The single-platform solution for all your AML

Our complete online compliance, risk management and education solution for accountants, legal firms and property businesses has already enabled 1000s to pass their supervisory visits.

In partnership with AML supervisors and professional bodies

Designed for regulated professionals,

by regulated professionals.

We know AMLCC works because we designed it to protect our own business. Just like our 15,000+ users, we use it every day to manage our AML and have used it to pass our supervisor’s visits.

Legal

Property

Accountancy

Achieve compliance

effectively and efficiently

Stay 100% compliant

Every process you need to meet all your legal obligations. At your fingertips.

Prove it instantly

PDF download. Complete audit trail. Remote supervisor access. Share your AML documents with your supervisor in seconds.

Enjoy peace of mind

Rest easy knowing you and your business are protected.

Improve efficiency by

managing your risk

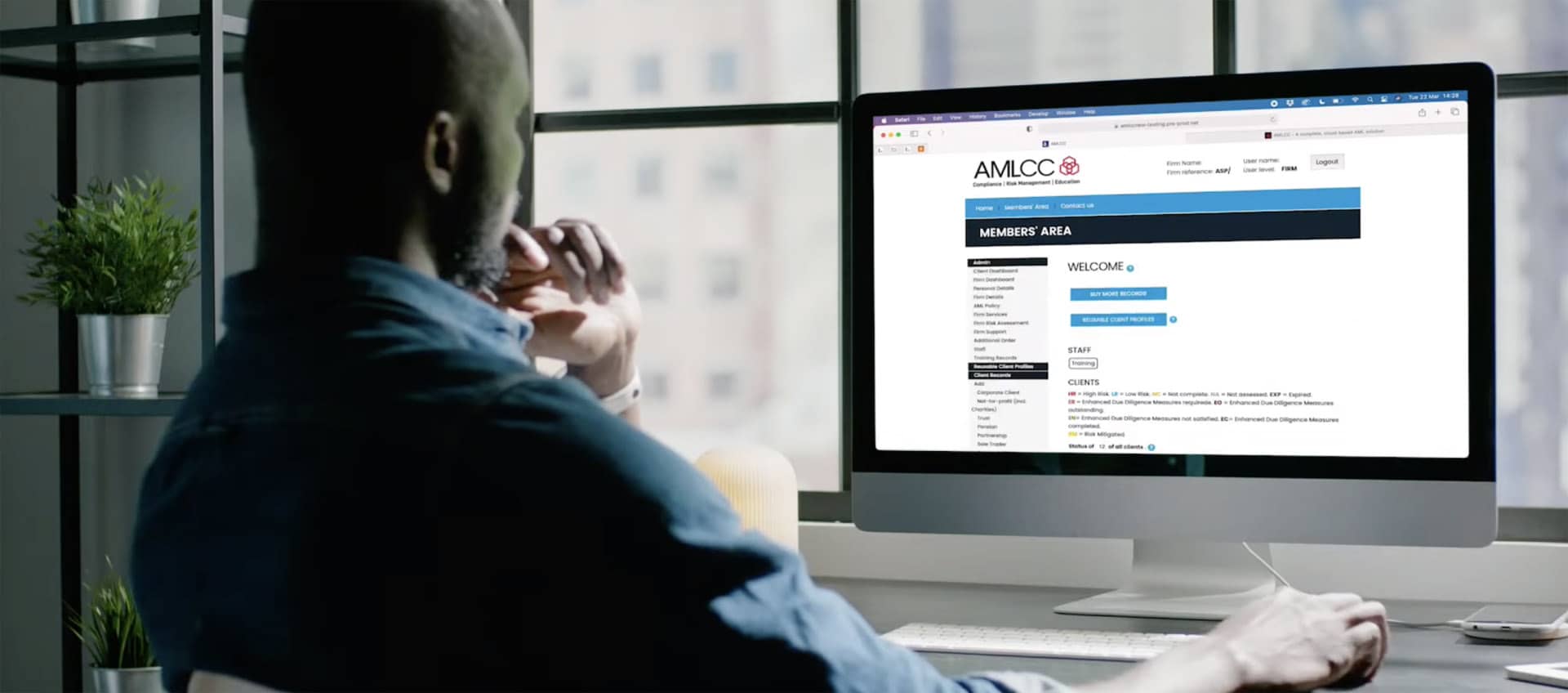

Take control

The central dashboard shows exactly where your business is at with its AML, minute by minute.

Balance workload

Know instantly where to allocate resources to suit your AML needs.

Ask the right questions

Targeted risk assessments for every organisation type make it easy to spot red flags.

Educate your teams

Build the correct knowledge base

Knowledge is power. Boost your employees’ ability to spot suspicious activity.

Minimise your training budget

All training videos are online and included in the AMLCC annual subscription.

Continuous learning

Site-wide guidance builds on knowledge and helps employees make the right decisions. Additional training on important topics including cyber-crime and crypto.

Read what we’re saying about the evolving AML landscape.

Everything in one place

Let’s get started

Stay secure with separate logins for your firm, MLRO, employees…

Get educated

Learn what you need to do, when you need to do it and how it protects you.

Document your business’ risk

Build bespoke business risk assessments by considering the risks your business faces.

Generate AML reports & documents

All your efforts result in supervisor-ready reports.

Live online AML environment

Manage live risks from the central dashboard.

The most important part

If there’s suspicion of money laundering, your team can report it.

Link clients together

Get a complete risk picture by linking clients and create your supervisor ready report.

Client due diligence

Risk assess every client for an accurate view of threats.

Features that work harder for you

| Supervisor endorsed | ||||||||

| Law Society partner | ||||||||

| All AML training in subscription | ||||||||

| Business-wide risk assessment | ||||||||

| 100% customisable, detailed AML policy | ||||||||

| Client risk assessments | ||||||||

| SAR portal to match NCA’s | ||||||||

| ID verification checks | ||||||||

| Link clients for transactions | ||||||||

| Live risk dashboard | ||||||||

| Audit trail | ||||||||

| Remote supervisor access | ||||||||

| Document management | ||||||||

| ICAEW technology accreditation | ||||||||

| Specific sector risks training | ||||||||

| Specific MLRO training |

Don’t just take our word for it…

“We had the man from the ICAEW here yesterday to carry out a QAD practice review. We got a clean bill of health – not a single action point…That is in no small measure due to AMLCC so I just wanted to say ‘thank you’”

“Thank you for such a perfect and informative [solution]. You have given me a clear direction for my AML training and CPD.”

“I just wanted to say ‘thank you’ to you, Richard, and all the team at AMLCC for providing a service that really does minimise the burden of AML compliance.”

“What a refreshing pleasure working with a company who actually listens to the feedback from their customers and communicates with them!”

“Your team they have been excellent from the moment Fiona did a demo for me with only 15 minutes notice, and thoroughly going through the AMLCC product, answering the many questions I had! It was at this point at which I made up my mind this is the sort of business I want to work with for my AML.”